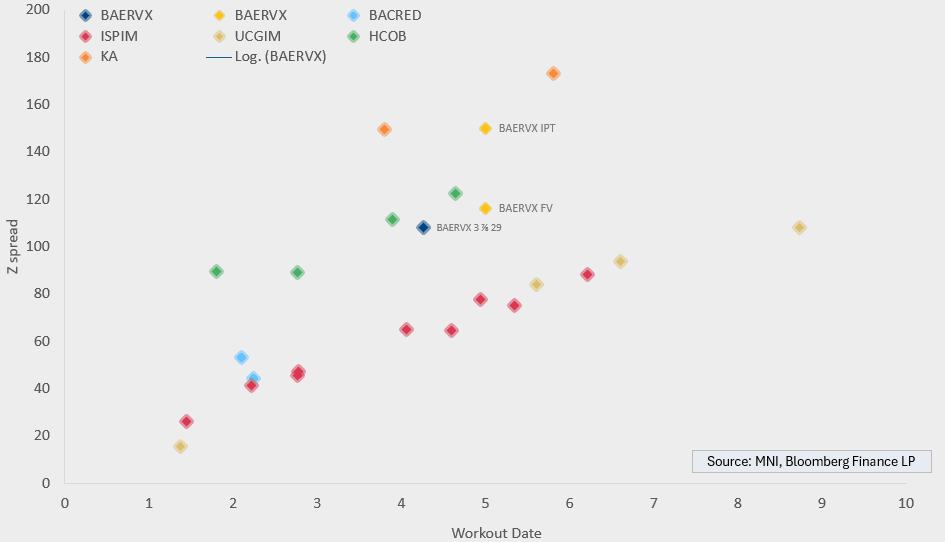

EU FINANCIALS: Julius Baer €500m WNG Sr Pref - FV

Jun-11 07:33

- IPT:MS+150 - Leads

- FV: MS+116 - 8bps wide of the BAERVX 3.875% 2029 for the 0.75 year extension. The existing bond widened 2-3bps relative WTD, so it is closer to 10bps wide of its pre mandate level.

- Exp. Ratings: Baa1

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Sell Off Extends As Risk Sentiment Improves

May-12 07:32

Gilts sell off on the moderation in Sino-U.S. trade tensions outlined elsewhere.

- News of a Putin-Zelenskiy meeting later this week also adds further background pressure.

- Futures as low as 91.69 before a recovery to ~91.90.

- Both the May 9 (92.07) & April 17 (91.73) lows were pierced, with next support located at the April 15 low (91.43).

- Yields 5-6bp higher, modest bear flattening bias on the curve.

- 2-Year yields trade as high at 3.98%, next upside area of interest located at the April 17 high (4.015%).

- 10s as high as 4.642%, next area of upside interest located at the April 15 high (4.672%).

- Hawkish moves in GBP STIRs extends, with ~51bp of cuts priced through year-end vs. ~54bp ahead of the gilt open.

- SONIA futures now flat to -8.5.

- Early focus this week will fall on the BoE Watchers’ conference and tomorrow’s labour market data, covered elsewhere. Expect our full labour market data preview to cross later today.

TARIFFS: Temporary US-China Tariff Cut Exceeds Expectations

May-12 07:30

(MNI) London - The escalating trade war between the US and China has, at least for now, entered a period of detente as both sides agree to a significant reduction in tariffs from their previous three-figure highs (see 'CROSS ASSET: Risk Surges as US/China Slash Tariffs for 90 Days', 0809BST). A joint statement outlining the reprieve comes after talks over the weekend in Geneva. Beforehand, these talks were viewed as initial discussions, unlikely to result in a notable breakthrough. Indeed, prior to the talks, US President Donald Trump had indicated that he viewed a tariff level of 80% as reasonable.

- The statement confirms that a mechanism has been established that will see talks continue. These will alternate in location between the US and China or a third country. The Chinese Ministry of Commerce says that it will adopt all measures to suspend or remove the non-tariff countermeasures taken against the US since 2 April. Both sides agree to lower tariffs for 90 days by 14 May.

- Speaking in Geneva, US Treasury Secretary Scott Bessent says there was "very good personal interaction, both sides represented [their] national interest well." Says that "neither side wants a [trade/economic] decoupling...neither side wants the equivalent of a trade embargo." Bessent: "We would like to see China open to more US goods"

- USTR Jamieson Greer confirms that tariffs related to the supply of fentanyl into the US will remain in place for now. Says fentanyl tariffs are "on [their] own track, but a very positive track, we are having very constructive conversations."

STIR: Hawkish ECB Repricing Following US/China Trade Talk Details

May-12 07:29

- Downside in Euribor futures extends after details of US/China tariff de-escalation are announced. Euribor futures are now -2.0 to -8.0 ticks through the blues, with the back of the whites/front of the reds leading the selloff.

- ECB-dated OIS now price 51bps of easing through year-end, almost 9bps more hawkish than Friday’s close. The implied probability of a rate cut in June remains almost 90% though.

- For the ECB, lower US/China tariffs imply a (i) smaller-than-expected negative global demand shock and (ii) potentially a lower risk of disinflationary Chinese trade diversion to the EU. Both of these dynamics work against dovish expectations for a terminal rate of below 1.75%. BBG's latest analyst survey sees a median terminal deposit rate expectation of 1.75% in September this year, with the most dovish forecast expecting a rate of 1.00% by December.

- It’s worth remembering that the latest tariff reprieve will only last 90 days though. In other words, policy uncertainty will remain elevated for at the next several months. Additionally, progress on a US/EU trade deal remains limited.

- Over the weekend, ECB Executive Board member Schnabel provided her arguments for holding rates at current levels. However, she did outline the conditions required for her to support more aggressive easing: “We would only need to react more forcefully to the tariff shock if we observed a sharp deterioration in labour market conditions or an unanchoring of inflation expectations to the downside”. See more in our earlier post.