JAPAN: Ishiba Restates Intention To Stay; Bettors Say 76% Chance PM Out In '25

Prime Minister Shigeru Ishiba again today indicated his intention to remain in office following the defeat of the governing coalition in the 20 July House of Councillors election. Speaking to reporters after a meeting with Economic Revitalisation Minister (and lead trade negotiator with the US) Ryosei Akazawa, Ishiba stated, "I would like to continue to do my utmost to dispel the concerns of domestic business operators and those working in related industries."

- Asahi Shimbun reports, "the Prime Minister emphasized, It is important that this agreement between the [US] President and I is implemented without fail," and stated his intention to do everything in his power to allay the concerns of domestic businesses when the contents of the agreement are implemented, again denying the idea of immediate resignation."

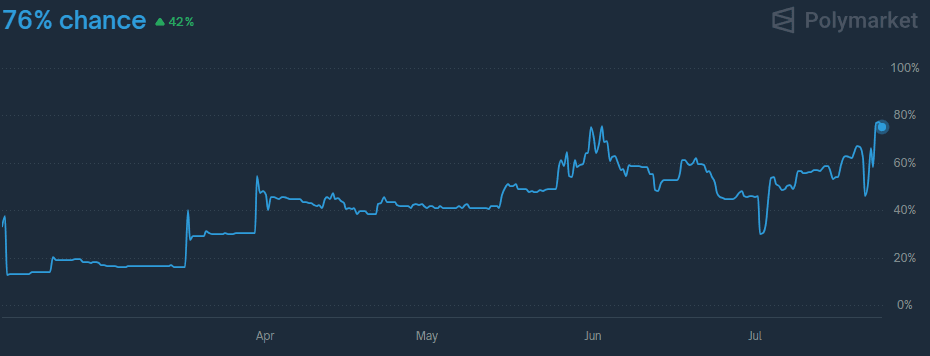

- Data from Polymarket shows political bettors assigning a 76% implied probability that Ishiba does not end the year as PM, up from a low of 31% at the start of July and 17% in March.

- Social conservative, fiscal populist Sanae Takaichi topped a post-election Yoimuri Shimbun poll, favoured by 26% of respondents to be the next PM.

- WSJ reported on 23 July, "The worst outcome for the Japanese yen would be if Sanae Takaichi became the next leader [...] “She is strongly ideologically aligned to former Prime Minister Shinzo Abe and his Abenomics policies of maintaining loose fiscal and monetary policies.” It would encourage speculation that the BOJ could face increased government pressure to delay interest-rate rises, weakening the yen, [MUFG] says."

Chart 1. Implied Probability Shigeru Ishiba Leaves Office in 2025, %

Source: Polymarket

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

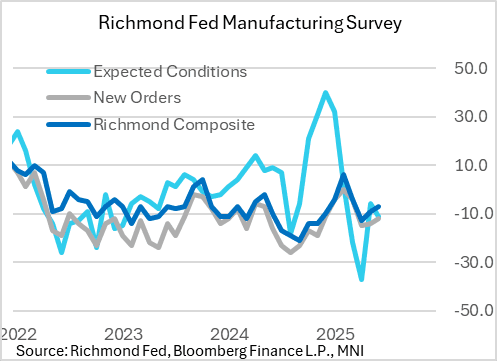

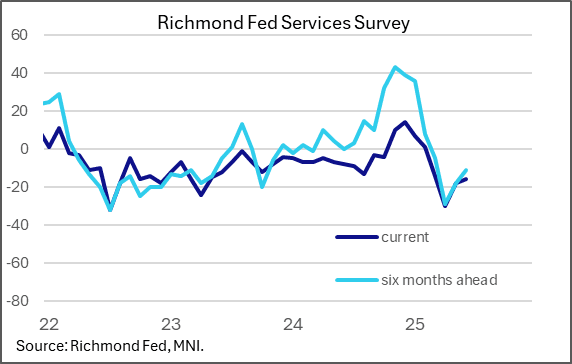

US DATA: Richmond Fed Regional Activity Stabilizing, Optimism Mixed (1/2)

The Richmond Fed's regional manufacturing and services surveys showed a modest pickup in activity in June vs May, but remained weak versus readings seen at the start of the year. Expectations were mixed-to-positive, with regional service sector respondents notably seeing a pickup in optimism. This is reflective of broader sentiment improving from the initial shock of the early April tariff announcements but suggests that improvements will be slow so long as uncertainty remains.

The composite manufacturing index was better than expected at -7 (-9 prior) vs consensus seeing a modest deterioration to -10, reflecting improvements in shipments and new orders but a deterioration in employment. The local business conditions index likewise improved to -20 from -25 though future expectations weakened. All of the major readings remained in negative territory, though this has become the norm over the last couple of years.

- On a stronger note, 6-month expectations moved or stayed positive for several activity categories including shipments and new orders; however even here this was mixed with weakening capex and equipment spending.

The service sector activity survey meanwhile saw the local business conditions index edge up to -16 from -18, with the revenues index up to -4 from -11 and the demand index rising to -7 from -8. employment and capex picked up slightly, but overall all of these indices remained weaker than Q1 levels.

- While current conditions, as with manufacturing, improved but remained weak, the 6-month expectations jumped: revenues to 20 (was 5) with demand 13 (was 2).

US TSYS: Curves Off Steeps as Bonds Lead Current Gains

- Treasury futures continue to extend gains, curves unwinding earlier steepener move as bond lead the charge, markets still digesting Fed Chairman Powell & Cleveland Fed Hammack's testimonies to the House.

- Currently, the Sep'25 10Y contract trades +7.5 at 111-22 (session high) focus on technical resistance at 111-26.5 (1.0% 10-dma envelope).

- Curves are coming off steeper levels: 2s10s +.204 at 48.221 vs. 51.322 high, 5s30s +2.401 at 98.430.

- Projected rate cut pricing has gained ground vs. morning levels (*), Dec at the reflecting most cuts since May 12: Jul'25 at -5.2bp (-5.7bp), Sep'25 at -25.8bp (-24.2bp), Oct'25 at -41.2bp (-39.7bp), Dec'25 at -59.4bp (-56.6bp).

- Cross asset roundup: Bbg US$ index near lows (BBDXY -8.12 at 1200.10; crude weaker (WTI -3.09 at 65.42), stocks inch higher (SPX Eminis +56.75 at 6133.75).

FED: Powell Again Implies That September FOMC Is Next Live Meeting

When asked at his House testimony about when we will see the inflation hit from tariffs, Powell implies that a cut isn't coming in July but there could be enough data by September's meeting to decide then (similar to his messaging at last week's FOMC press conference):

- "The things that are being sold at retail now, they might have been put into into inventory before the tariffs in February or March. So we think we should start to see this over the summer, in the June numbers, and in the July numbers. And if we don't... it may turn out that the pass through is less or more than we think. And I think we're going to be learning...we'll get an inflation number for June, we'll learn something, then we'll get it for July, as we go through the summer, we should start seeing this and if we don't, I think we're perfectly open to the idea that the passthrough will be less than we think, and if so, that'll matter for our policy."