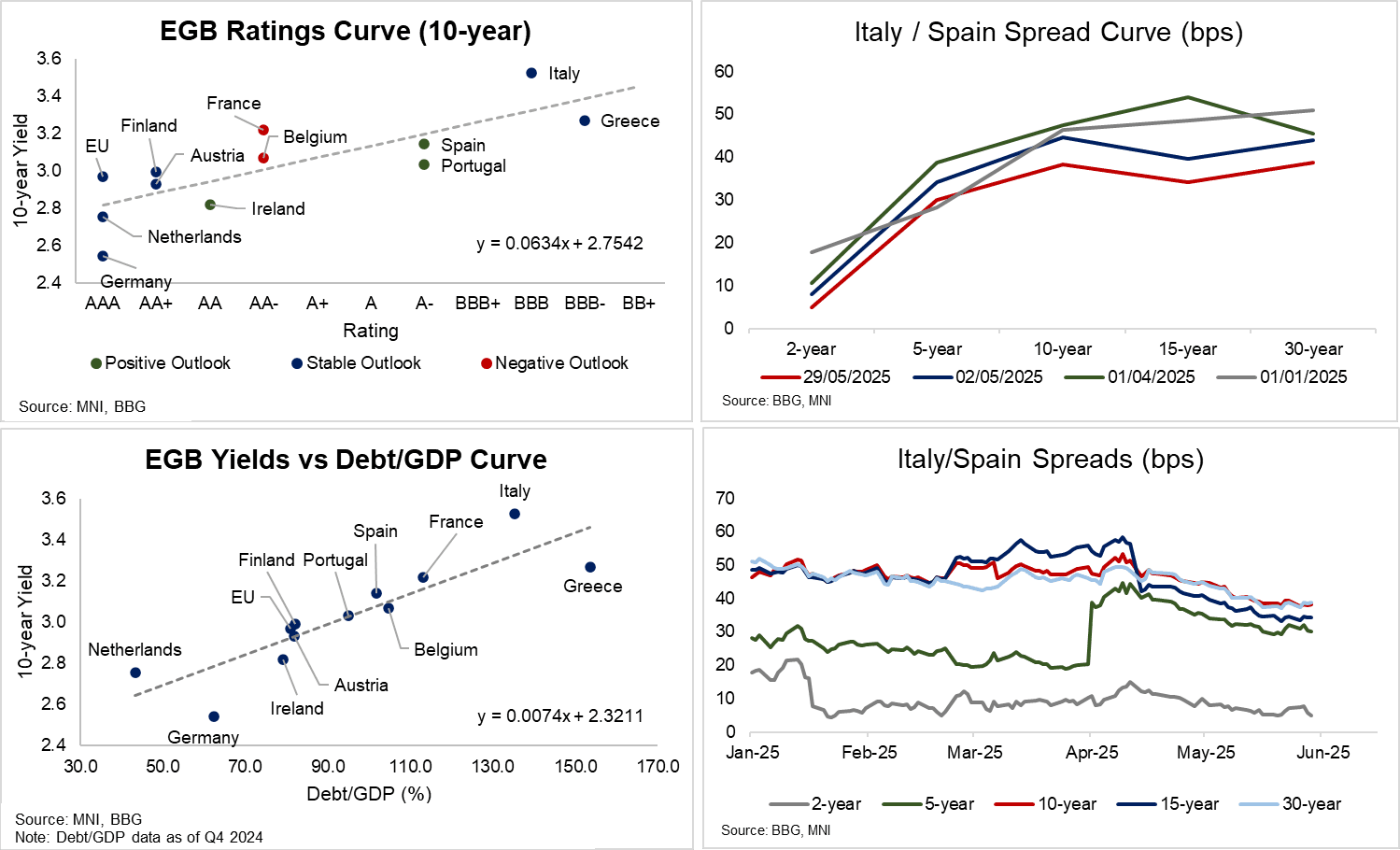

EGBS: Fundamentals Point To Unwind Pressures for Recent Italy/Spain Narrowing

BTPs have not just outperformed Bunds in recent weeks, but also Southern European peers such as Spanish Bonos/Oblis. That’s despite Spanish fiscal/economic fundamentals still appearing more favourable than in Italy. As such, there may be scope for some unwind of recent Italy/Spain spread narrowing.

- Long BTPs vs EGB peers has been a popular trade since phase of Liberation Day volatility, with the fall in US effective tariff rates supporting a recovery in broader risk sentiment. A move towards (and through) the 100bp handle in the 10-year BTP/Bund spread has provided additional momentum for Italian paper’s relative outperformance.

- SPGB underperformance against BTPs has been most notable at the 15-year maturity, with the BTP/SPGB spread tightening from 54bps to 34bps since the start of April (i.e. just before Liberation Day). The spread traded at 48bps at the start of this year.

- The 5-year maturity has also tightened 9bps since the start of April to 30bps, but sits a touch wider than the 28bps seen on January 1.

- While Italy displayed impressive fiscal consolidation through last year (the budget deficit was -3.4% compared to a -3.8% government forecast), supporting more positive ratings action, its fundamentals still appear less surefooted relative to Spain: the EC projects the Italian deficit at 3.3% in 2025 and 2.9% in 2026. The Spanish deficit is seen at 2.8% in 2025 and 2.5% in 2026 (from 3.2% in 2024). While Italian growth is expected to remain below 1% through 2026, Spanish growth is still seen at 2.0% in 2026.

- Both Fitch and Moody’s have Spanish and Italian ratings on a Positive Outlook, but the next scheduled reviews are not due until September/October this year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Mixed SOFR Midcurve Call Structures

- -8,000 0QM5 96.87/97.00/97.25/97.3 call condors, 2.87 ref 96.98

- +2,500 0QM5 97.50/98.00/1000 2x3x1 call flys 7.0 vs. 96.365/0.14%

US OUTLOOK/OPINION: Atlanta Fed Gold-Adjusted Nowcast At New Low For Q1

The latest and final gold-adjusted Atlanta Fed GDPNow estimate for Q1 growth is a new low going into tomorrow's GDP print, on the back of the much larger than expected March goods trade deficit offset slightly by higher inventory change estimates.

- "The final GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2025 is -2.7 percent on April 29, down from -2.4 percent on April 24. The final alternative model forecast, which adjusts for imports and exports of gold is -1.5 percent. After this morning’s Advance Economic Indicators release from the US Census Bureau, the standard and alternative model nowcasts of the contribution of net exports to first-quarter real GDP growth declined from -4.90 percentage points and -2.85 percentage points, respectively, to -5.26 percentage points and -4.05 percentage points."

- This is much more negative than the 0.3% growth figure for Q1 growth expected by consensus in Wednesday's release.

STIR: Euribor Curve Prices In Hikes From Q2 ’26; But May Be Too Hawkish

Although the market is currently focused on how many more cuts the ECB will deliver and the speed in which it reaches the terminal rate, attention will soon shift to assessing whether rate hikes are plausible in 2026. Some analysts have already pencilled hikes into their baseline projections, e.g. UBS see 50bps of hikes in late 2026.

- The ER H6 / Z6 spread is currently 16.5 ticks, off the April 9 high of 21.0 ticks. These levels crudely imply a ~65% probability of an ECB hike between Q2-Q4 2026 (for now abstracting from the liquidity/credit component embedded within Euribor futures).

- While it is reasonable to assume a 2026 hike is more likely than a cut at this stage, current pricing may still be considered too hawkish, given uncertainty around whether higher trade barriers and German fiscal spending will be inflationary in the medium-term.

- On the first channel, higher trade barriers may not culminate in higher Eurozone inflation if (1) Chinese disinflationary trade diversion is material, (2) EU retaliation against the US is limited and (3) the real effective Euro holds onto or extends recent strength.

- Meanwhile, the hawkish-leaning Bundesbank President Nagel suggested on April 23 that the German fiscal package will not be inflationary. Analyst forecasts submitted to BBG also do not yet incorporate a material uptick in 2026 German inflation.

- The current Euribor-implied terminal rate is 1.66%, indicated by the H6 contract. That’s off the recent dovish closing extreme of 1.58% on April 22, but still well above the 1.94% just before the April 2 US tariff announcement and the 2.16% following the German fiscal announcement/March ECB decision.