EM CEEMEA CREDIT: First Quantum: headlines hitting tape, conf call on

Jul-24 13:18

"*FIRST QUANTUM SEES NO DIRECT IMPACT FROM US COPPER TARIFFS" - BBG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

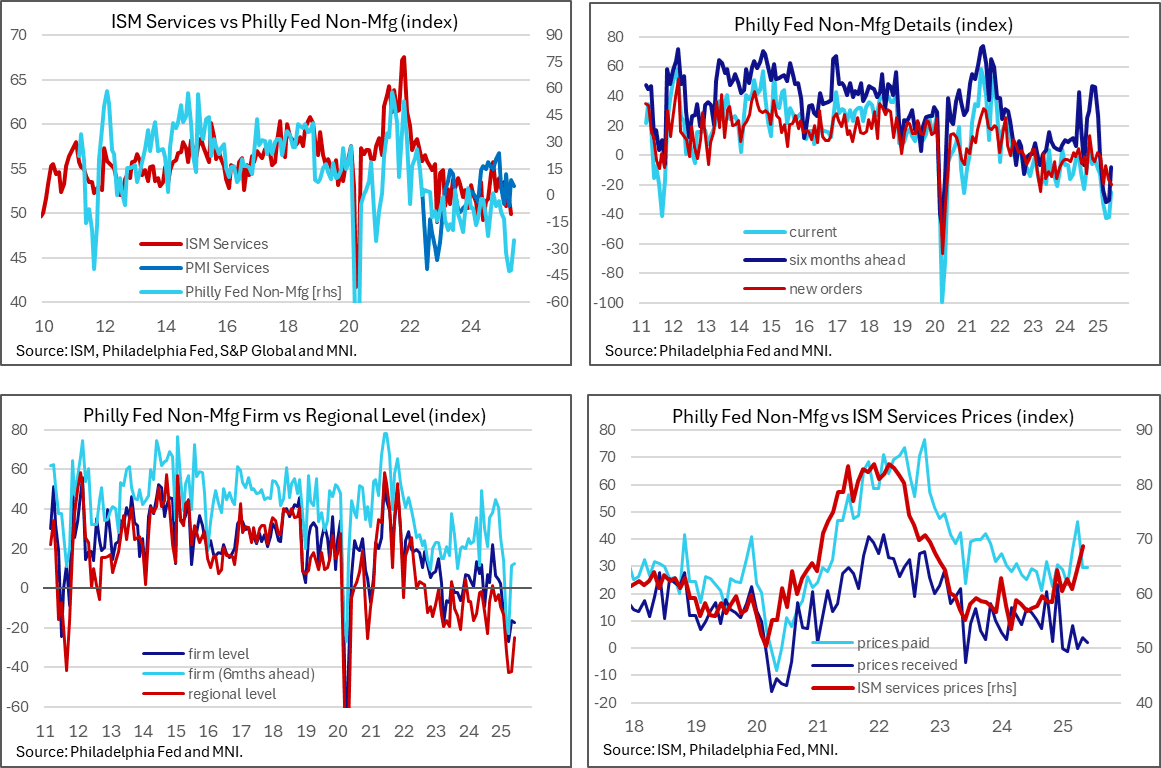

US DATA: Philly Fed Non-Mfg Improves As Regional Weakness Dialled Back

Jun-24 13:11

The Philly Fed non-manufacturing survey saw firms dial back particularly negative views on the regional economy to one closer to their own experiences. Some details were weak however, such as new recent lows for new orders along with the prices received index almost in balance.

- The Philly Fed non-manufacturing index improved to -25.0 in June after two particularly weak readings of -41.9 in May and -42.7 in April (both the weakest since the series started in 2011 aside from two months at the depths of the pandemic).

- For context though, this is the highest since February and compares poorly with an average -8.0 in 2024, -10.4 in 2023 and +3.7 in 2022.

- Recent swings in sentiment have been more pronounced for this measure of regional perceptions, whilst the firm-own activity index has been steadier. This own look at activity was little changed at -17.3 after -16.3 in May having recovered from lows of -26.7 in April after tariff announcements (also the lowest in the series aside from Apr/May 2020).

- The details behind these headline figures were mixed, but new orders weakness was notable, falling from -16.3 to -20.1 for its lowest since Apr 2023 and before that the pandemic.

- This new orders weakness contrasts with yesterday’s flash PMIs, which indicated a softening but one that remains in positive territory: “The ongoing expansion reflected a further rise in new orders, which have now risen continually for 14 months, though the rise in orders dipped slightly in June to remain well below the strong gains seen at the turn of the year. Similar gains in inflows of new work were recorded in the manufacturing and service sectors and, in both cases, growth was driven by rising domestic demand.”

- As for price components, prices paid held steady at 29.7 in June after 29.6 in May, off April’s 46.5 for levels close to last year’s 28.3 average. However, there’s still sign of feed through to prices received with the index at 2.2 after 4.0 in May, down from the 11.4 averaged last year.

US TSYS: Post-House Price React

Jun-24 13:07

- Treasuries bounce slightly, remain weaker after latest round of higher than expected house price data.

- Markets holding narrow range with main focus on Fed Chairman Powell's semiannual testimony to House at 1000ET - not to mention Iran/Israel headline watching.

- Currently, Jun'25 10Y trades -7 at 111-07.5 (111-06L / 111-14.5H), heavier volumes: TYU5 over 664,000.

- Technical support below at 110-21.5 (50-day EMA).

- Curves moving steeper: 2s10s +2.262 at 50.279; 5s30s +3.304 at 99.333.

EURGBP: BofA Still Look For EUR/GBP Lower Med-Term, Despite Seasonal Uptick

Jun-24 13:03

Bank of America note that GBP underperformance in June has become a seasonal theme in recent years.

- However, they note there is “little visibility of the precise drivers” of the seasonal move higher in EUR/GBP.

- They maintain their EUR/GBP medium-term view of 0.75-0.80, though concede that risks to the call have risen.

- They note that “UK data appears to have been bearing the impact of tariff uncertainty earlier than in Europe, whilst a terms of trade shock is likely to disproportionately impact Europe more than the UK given recent history”.

- BofA also highlight that “consensus UK growth forecasts have improved in recent weeks as consumer headwinds ease”.

- They also note the recent (seasonal, flow-driven) bid has generated “a notable dislocation between EUR/GBP and some of its traditional anchors”, rate spreads & FX volatility. Furthermore, they highlight that EUR/GBP skew has not shifted meaningfully against GBP through recent weakness.