EMISSIONS: EU Mid-Day Carbon Summary: EUAs Edge Up W/W, UKAs Fall

Oct-10 11:12

EUAs are tracking small weekly gains, while UKAs are still tracking a week-on-week decline after last week’s rally fuelled by progress on an EU-UK CBAM deal

- EUA DEC 25 up 0.8% at 79.83 EUR/MT

- ICE UKA Dec25 up 0.8% at 55.43 GBP/MT

- NBP Gas NOV 25 down 1% at 82.11 GBp/therm

- TTF Gas NOV 25 down 1.4% at 31.91 EUR/MWh

- Rotterdam Coal NOV 25 up 0.3% at 91 USD/MT

- TTF front month is down from a high of €33.615/MWh on Oct. 7 but still holding a net gain on the week weighing Ukrainian gas infrastructure disruption with lower geopolitical risk from the Middle East.

- The latest German EUA CAP3 auction cleared at €79.22/MWh, compared with €77.95/ton CO2e in the previous auction on 9 October according to EEX.

- EUA prices are expected to edge higher as the market shifts focus to a tightening year-ahead supply–demand balance, according to Volue.

- Citepa estimates France will reduce emissions by 0.8% in 2025, falling short of the country’s targets.

- Germany’s Chancellor Friedrich Merz said he will seek to prevent a strict end to new combustion engine vehicle sales from 2035, following talks with car industry representatives on Thursday.

- Malaysia’s government announced on Friday it will introduce a carbon tax on iron, steel and the energy sector in 2026, in anticipation of the EU’s CBAM.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SWEDEN: 2026 Budget Policies Continue To Filter Through

Sep-10 11:11

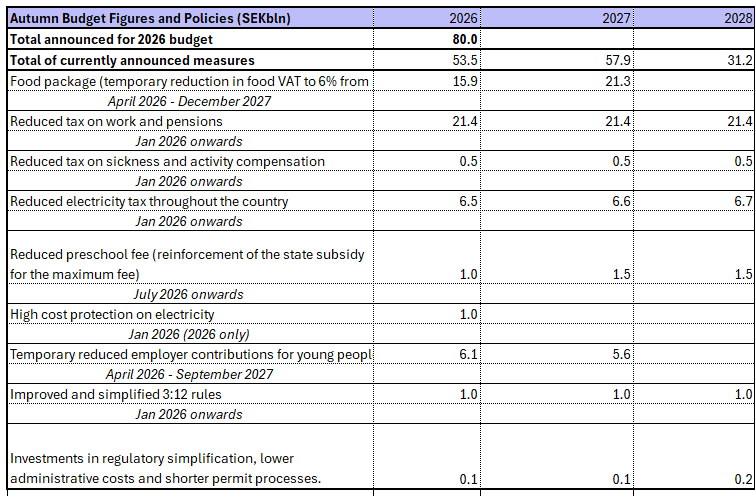

This morning, the Swedish Government announced the latest set of measures included in the 2026 budget (to be presented in full on Sep 22). Today’s focus was an “entrepreneurship package”, the first set of business-focused policies entering the budget after several household-centred announcements in recent days.

- The Finance Ministry has now announced SEK53.5bln of expansionary policies for 2026, out of a SEK80bln total earmarked for the budget.

- Today’s policies totalled SEK7.2bln for 2026. The majority (SEK6.05bln) is being spent on a temporary reduction in the employer costs associated with hiring 18-23 year olds. See here for more.

- The Swedish labour market remains weak, so measures aimed at supporting businesses to stimulate employment appear necessary. A press conference detailing education and labour market-specific policies in the 2026 budget is currently ongoing (see here)

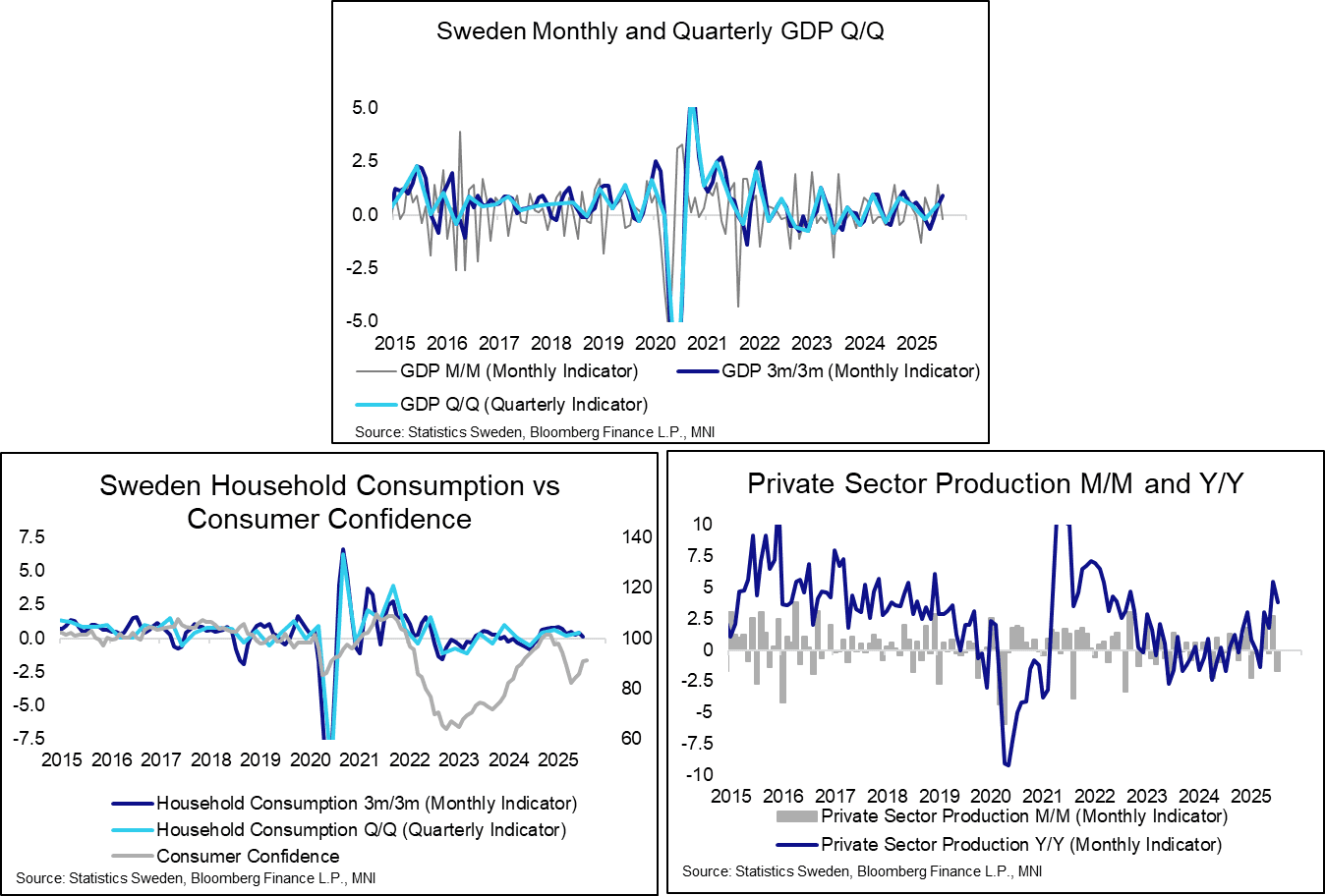

- Monthly activity indicators were released this morning. There are tentative signs of improvement for GDP/production as a whole, but consumption signals remain soft:

- GDP fell 0.2% M/M, but June’s figure was revised up to 1.4% from 0.5% initial (as expected following the Q2 final GDP report last month). On a 3m/3m basis, GDP is up 0.9% (vs 0.5% in June).

- Household consumption rose 0.2% M/M (vs 0.6% prior), but 3m/3m growth fell to 0.1%, the weakest since August 2024.

- Private sector production fell 1.7% M/M, unwinding a portion of June’s solid 2.7% rise. On an annual basis, production is up 3.8%.

OUTLOOK: Price Signal Summary - EURUSD Trend Theme Remains Bullish

Sep-10 11:02

- In FX, the trend theme in EURUSD remains bullish. Resistance at 1.1743, the Aug 22 high, has been cleared reinforcing a bull cycle. This signals scope for an extension towards 1.1829, the Jul 01 high and bull trigger. Clearance of this hurdle would confirm a resumption of the primary uptrend. Support to watch is around the 50-day EMA, at 1.1628.

- GBPUSD is holding on to its gains since rallying off the Sep 3 low. The climb has retraced the steep sell-off on Sep 2 and highlights a stronger bullish development. This also suggests the corrective cycle between Aug 14 - Sep 3 is over. Sights are on resistance at 1.3595, the Aug 14 high and a bull trigger. A break would strengthen a bullish condition. Initial support to watch is 1.3465, the 50-day EMA.

- USDJPY continues to trade inside a range. Attention is on key short-term support at 146.21, the Aug 14 low and a bear trigger. A break of this level would signal a stronger bearish threat and highlight a range breakout. This would expose 145.40, 50% of the Apr - Aug upleg. On the upside, clearance of 149.14, the Sep 3 high is required to reinstate a bullish theme.

MNI: US MBA: MARKET COMPOSITE +9.2% SA THRU SEP 05 WK

Sep-10 11:00

- MNI: US MBA: MARKET COMPOSITE +9.2% SA THRU SEP 05 WK

Trending Top

Jun-26 16:22