BONDS: EGBs-GILTS CASH CLOSE: Pressure Continues

EGBs and Gilts remained under pressure Thursday. * After a back-and-forth start, yields rose to ses...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBPUSD TECHS: Monitoring Resistance At The 50-Day EMA

- RES 4: 1.3658 High May 1 and a key resistance

- RES 3: 1.3574 76.4% retracement of the May 1 - 18 bear leg

- RES 2: 1.3522 61.8% retracement of the May 1 - 18 bear leg

- RES 1: 1.3480/1.3509 61.8% of the May 1 - 18 bear leg/ High May 26

- PRICE: 1.3422 @ 16:31 BST Jun 16

- SUP 1: 1.3384/3303 Low Jun 12 / Low May 18 and the bear trigger

- SUP 2: 1.3277 76.4% retracement of the Mar 31 - May 1 bull leg

- SUP 3: 1.3212 Low Apr 7

- SUP 4: 1.3159 Low Mar 31 and a key support

Recent gains in GBPUSD resulted in a breach of the 50-day EMA, at 1.3442. However, this EMA as a resistance, remains intact for now. A clear break of it would signal scope for a continuation higher towards 1.3509, the May 26 high and a bull trigger. Clearance of this hurdle would highlight a stronger reversal. For now trend signals remain bearish. Key short-term support is 1.3303, the May 18 low. Clearance of this level would be a bearish development.

ECB: Makhlouf Warns On Potential For Lingering Price Pressures

ECB’s Makhlouf has warned in a speech (link) that price pressures could linger despite a US-Iran peace deal, coming from a Governing Council member who is somewhat hawkish leaning but certainly not at the most hawkish end of the spectrum. ECB-dated OIS has 5bp of hikes priced for the July meeting before a cumulative ~20bp with the projection meeting in September vs the full pricing of a hike for the latter on Friday before the US-Iran agreement.

- “[A]n end to the conflict does not necessarily mean an immediate end to the shock. The balance of risk in staff projections – that is considering the mild-to-severe scenarios I outlined – showed that a rate increase in June was the right approach to bring inflation back to our 2% target over the medium term.” The latter echoes Lagarde’s point from Thursday’s press conference that a hike was robust even in the newly introduced mild scenario.

- “It remains to be seen how quickly supply chains normalise and energy prices adjust. The direct price pressures might not fade so quickly if the infrastructure damage from the war means production only recovers with a lag. Then there is the question of shipping through the Strait of Hormuz, on which there remains little clarity.”

- “So, despite the recent and relatively positive news, we really need clarity around energy supply. And until then, I continue to monitor the pass-through of the shock, focusing on the indirect and second-round effects I have described.”

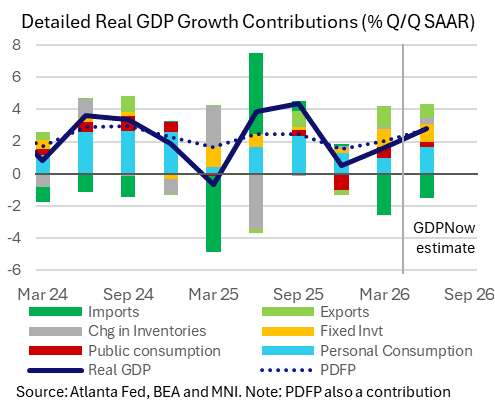

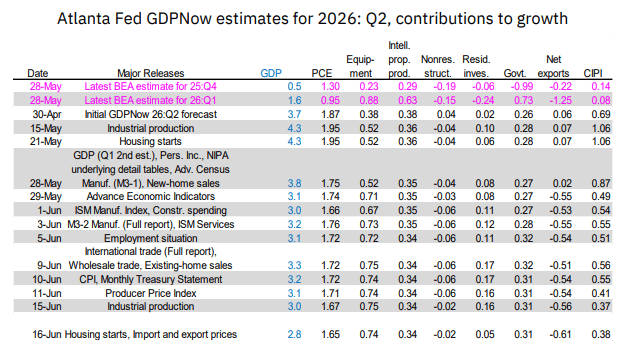

US DATA: GDPNow Marked Down To Softest Of Q2 Vintage

The Atlanta Fed’s GDPNow for real GDP growth in Q2 has been revised from 3.3% to 2.8% annualized since its last update a week ago, driven by various releases but with the largest single step from soft housing starts. PDFP is still seen accelerating to a solid 3.1-3.2% in Q2 however, which if accurate would be its strongest quarter since 3Q24.

- GDPNow has seen a reasonable trimming in Q2 real GDP tracking to 2.83% annualized from 3.29% in its last update from Jun 9, marking a new low for Q2 tracking.

- Details suggests a steady drip feed of negative revisions from various releases over that time although with the largest step coming from today’s weak housing starts release (from 3.0% to 2.8%).

- It would still mark an acceleration from the 1.6% in Q1 and 0.5% in Q4 as real GDP growth continues to have seen sizeable swings after a particularly volatile 2025 (averaging 2.0% but with a range of -0.65% in 1Q25 to 4.4% in 3Q25).

- Private domestic final purchases (PDFP) continues to give a better sense of underlying demand in the economy and is currently seen increasing circa 3.1-3.2% vs 3.3% prior to last week’s update. That would be an acceleration from the 2.4% in Q1 and also averaged through 2025.

- As for some key drivers since the last update, PCE is seen increasing 2.4% vs 2.5% prior (1.4% in Q1) whilst equipment investment is still seen jumping another 13.8% vs 14.0% prior (17.2% in Q1). The hit unsurprisingly comes from residential investment now seen rising just 1.3% annualized vs 4.3% prior for a tepid bounce after the -6.3% in Q1.

- Latest expected contributions: PDFP seen adding 2.8pp after 2.1pp in Q1 (of which overall non-resi invt seen at 1.1pp after 1.35pp and PCE at 1.65pp after 0.95pp), government 0.3pp after 0.7pp, changes in inventories 0.4pp vs 0.1pp and net exports -0.6pp vs -1.25pp.