OIL: Distillate-Rich Brazilian and Guyanese Barrels Rallying

Prices of distillate-rich barrels from Brazil and Guyana are having a rare rally this summer, a period when fuelmakers typically bid up grades better suited to producing gasoline, Bloomberg reports.

- Both Brazilian Tupi and Guyanese Liza oil have flipped to premiums to Dated Brent, compared with discounts a few months ago, as diesel inventories hover near multi-decade lows.

- Tupi recently traded at a premium of around 60 cents a barrel to Dated Brent on a FOB basis from ports in Brazil, compared with a discount of 70 cents a month ago, according to Bloomberg sources.

- Medium-sweet Liza oil is quoted at a premium of 65 cents, compared with a discount two months ago, also on an FOB basis.

- Those differentials are strengthening even despite falling flat oil prices, Bloomberg says.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Midday Equities Roundup: IT, Financials & Communications Lead Gainers

- Stocks are holding moderate gains Tuesday as geopolitical headlines and Fed speakers offered alternating distraction and modest support in late morning trade.

- Currently, the DJIA trades up 419.72 points (0.99%) at 43005.98, S&P E-Minis up 59.5 points (0.98%) at 6136.5, Nasdaq up 268.3 points (1.4%) at 19899.68.

- Information Technology, Financials and Communication Services sectors led gainers in the first half: IT leaders included Intel +5.69%, Advanced Micro Devices +5.56%, Super Micro Computer +4.65% and Enphase Energy +4.54%

- Services stocks led the Financials sector: Coinbase Global +9.38%, Apollo Global Management +3.78% and KKR & Co +3.32%, while media and entertainment shares supported the Communication Services sector: Warner Bros Discovery +2.95%, Charter Communications +2.27%, Netflix +1.96% and Match Group +1.78%

- On the flipside, weaker crude prices (WTI -3.2 at 65.31) weighed on oil and gas stocks: Occidental Petroleum -2.37%, Exxon Mobil -2.06%, Chevron -1.71%, Hess -1.70% and ConocoPhillips -1.20%.

- Broadline retailers and personal products maker underperformed: Dollar General -1.82%, Estee Lauder -1.50%, Dollar Tree -1.49% and Colgate-Palmolive -1.30%.

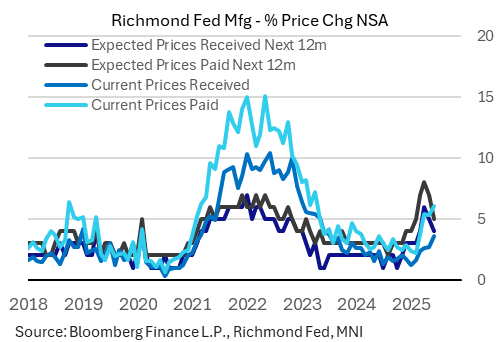

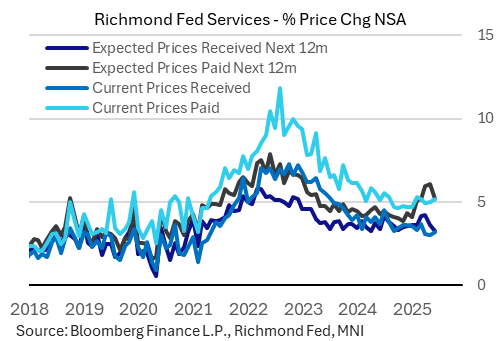

US DATA: Richmond Fed Survey Suggests Tariff Inflation Still Emerging (2/2)

The Richmond Fed's manufacturing and services surveys showed a divergence in inflation dynamics in June, with current prices reportedly higher but expected future inflation pulling back after recent peaks.

- Manufacturing firms saw current prices received and paid rise, but expected prices continue to pull back, while services firms saw expected future prrices increase even as current inflation pulled back.

- Starting with manufacturing, current prices paid hit a fresh 26-month high 6.1% (based on reported inflation over the last 12 months) , up from 2.2% as recently as February, while prices received rose to a 23-month high 3.6% (up from 1.2% recent low in Jan). But expected prices pulled back for a second consecutive month: paid to 5.0% (4-month low, vs 8.0% peak in April) and received 4.0% (3-month low, ve 6.0% April peak).

- For services firms, current prices ticked up, both received (3.2%, a 3-month high) and paid (5.2%, joint-highest in 4-months). Expected prices however pulled back sharply: paid to 5.2% (3-month low, down from May's recent peak of 6.0%) with received down to 3.2% (14-month low, down from 4.2% recent peak in Mar-Apr).

- We wouldn't read too much into these month-to-month dynamics but they possibly indicate that pipeline price pressures from tariffs are feeding through to regional firms, though the future inflation isn't quite as bad as had been feared immediately after April's Liberation Day announcement.

- In general, services inflation looks better-contained than that for manufactured goods.

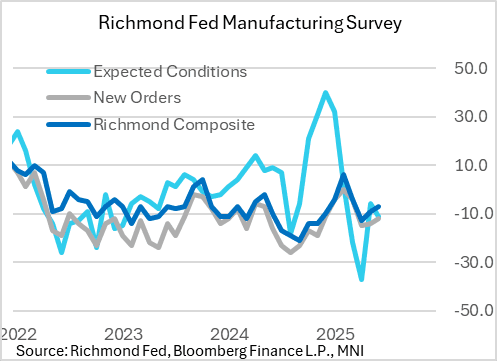

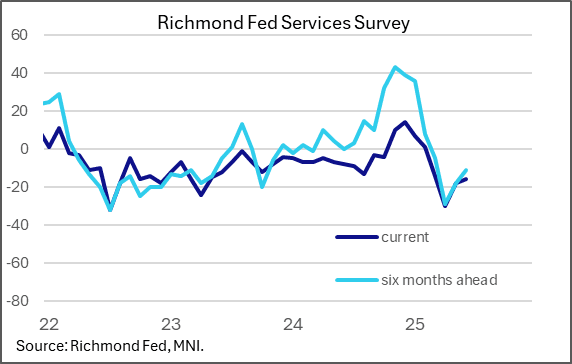

US DATA: Richmond Fed Regional Activity Stabilizing, Optimism Mixed (1/2)

The Richmond Fed's regional manufacturing and services surveys showed a modest pickup in activity in June vs May, but remained weak versus readings seen at the start of the year. Expectations were mixed-to-positive, with regional service sector respondents notably seeing a pickup in optimism. This is reflective of broader sentiment improving from the initial shock of the early April tariff announcements but suggests that improvements will be slow so long as uncertainty remains.

The composite manufacturing index was better than expected at -7 (-9 prior) vs consensus seeing a modest deterioration to -10, reflecting improvements in shipments and new orders but a deterioration in employment. The local business conditions index likewise improved to -20 from -25 though future expectations weakened. All of the major readings remained in negative territory, though this has become the norm over the last couple of years.

- On a stronger note, 6-month expectations moved or stayed positive for several activity categories including shipments and new orders; however even here this was mixed with weakening capex and equipment spending.

The service sector activity survey meanwhile saw the local business conditions index edge up to -16 from -18, with the revenues index up to -4 from -11 and the demand index rising to -7 from -8. employment and capex picked up slightly, but overall all of these indices remained weaker than Q1 levels.

- While current conditions, as with manufacturing, improved but remained weak, the 6-month expectations jumped: revenues to 20 (was 5) with demand 13 (was 2).