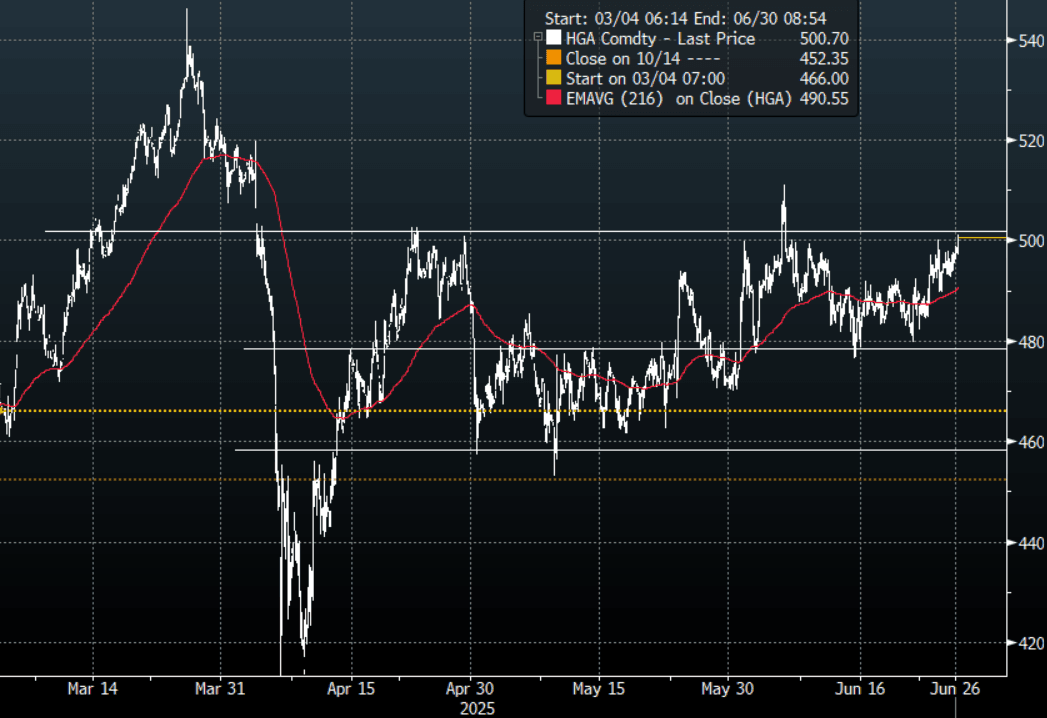

METALS: Copper - HGU5 Probing Above 500.00

Jun-26 03:04

The range overnight for the HGU5 contract was 492.60 - 498.50, Asia is currently trading around 500.90.

- The LME cash market closed overnight around 9878.00.

- (Bloomberg) - Copper extended gains for a fifth day, after Goldman Sachs Group Inc. said it expected prices to rise to a 2025 peak of around $10,050 a ton in August, as supplies outside the US tighten.”

- “The ex-US copper market has tightened, causing fears of a regional copper shortage despite the global market currently being in surplus,” Goldman analysts including Eoin Dinsmore wrote in a note on Thursday.”

- “Prices are expected to keep rising due to tariff-driven reductions in stock outside the US and relatively resilient Chinese sentiment and activity”

- The decline in inventories and a USD back under pressure has seen Copper look to probe above the 500 area once more.

- A sustained break back above $500.00 and the move higher could potentially gain momentum and to trend higher.

Fig 1 : Copper(HGN5) Hourly Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Richer With US Tsys, April CPI Tomorrow, Retail Sales on Friday

May-27 02:58

ACGBs (YM +3.0 & XM +5.0) are stronger with US tsys 1-3bps richer in today’s Asia-Pac session after yesterday’s holiday.

- Cash ACGBs are 3-5bps richer with the AU-US 10-year yield differential at -16bps.

- The bills strip richer, with pricing +1 to +3.

- RBA-dated OIS pricing is showing a 25bp rate cut in July as a 73% probability, with a cumulative 75bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Today, the local calendar has been light. The ANZ-Roy Morgan Consumer Confidence Index fell to 87 in the week of May 19 to May 25 from 88.8 in the prior week.

- The focus remains on tomorrow’s April CPI, which is forecast to moderate to 2.3% y/y from 2.4%. The trimmed mean has been around 2.7% y/y for four consecutive months. There will be limited updates to the services components being the first month of the quarter.

- Some of the components of Q1 GDP are also released this week, namely construction (Wed) and private capex (Thu).

- April retail sales print on Friday and are projected to rise 0.3% m/m after increasing the same amount in March.

CHINA: Bond Futures Lower

May-27 02:44

- China bond futures are marginally lower today, following the injection of liquidity during the OMO.

- The 10YR future is down -0.05 at 108.80 having bounced off the 20-day EMA of 108.84.

- The 50-day EMA sits below at 108.73.

- The 2YR future is down -0.02 at 102.40 and remains below all major moving averages. The nearest being the 20-day EMA of 102.46.

- The 10YR CGB is higher by +0.05bp today at 1.69%

- Industrial Profits for April were released today and continue to trend in the right direction, improving on March.

- Next key data will be Official PMIs on the 31st.

STIR: RBNZ-Dated OIS Fully Priced For Tomorrow’s Meeting

May-27 02:39

RBNZ-dated OIS pricing was little changed across meetings today.

- Markets continue to price in 25bps of easing for tomorrow’s meeting, with 64bps expected by November 2025.

- However, rates remain 2–19bps higher than levels observed prior to the Q1 CPI release on April 17.

- Amid firmer NZ rates and softer Australian rates—following last week’s dovish RBA pivot and rate cut—the expected year-end policy rate differential between Australia and New Zealand has narrowed by 20–25bps over the past week, currently standing at +22bps.

Figure 1: RBNZ Official Rate Profile Vs. Expected Dec-25 Level

Source: MNI - Market News / Bloomberg