EM LATAM CREDIT: Comison Ejecutiva Hidroelectrica Rio Lemp: New Issue Fair Value

(B3/B-)

"NEW DEAL: Comison Ejecutiva Hidroelectrica $Bmark Long 7Y" – Bbg

IPTs Long 7Y: 9% Area

FV Long 7Y: 9% Area

• Government owned electric utility known as CEL proposed issuing a USD benchmark senior unsecured long 7-year guaranteed by the Republic of El Salvador.

• Republic of El Salvador (ELSALV; B3/B-/B-) 2035 notes were quoted 8.32% while the ELSALV 2032s were quoted 8.04%. If we interpolate for a new long 7-year El Salvador plus a new issue concession we see fair value at 8.5%. We can add about 50bp for a government owned utility issue, as shown below, to derive a fair value for this new issue of 9%.

• To judge the spread over the sovereign for a government owned utility we can look to Costa Rican government owned utility Instituto Costarricense de Electricidad (COSICE; Ba2/NR/BBpos) that is quoted about 55bp wide to the Costa Rica sovereign (COSTAR; Ba3pos/BB-pos/BBpos) in both the 2031 and 2043 maturities.

• The notes have an unconditional and irrevocable guarantee of scheduled principal and interest on the bonds provided by the Government of El Salvador, according to Moody’s.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

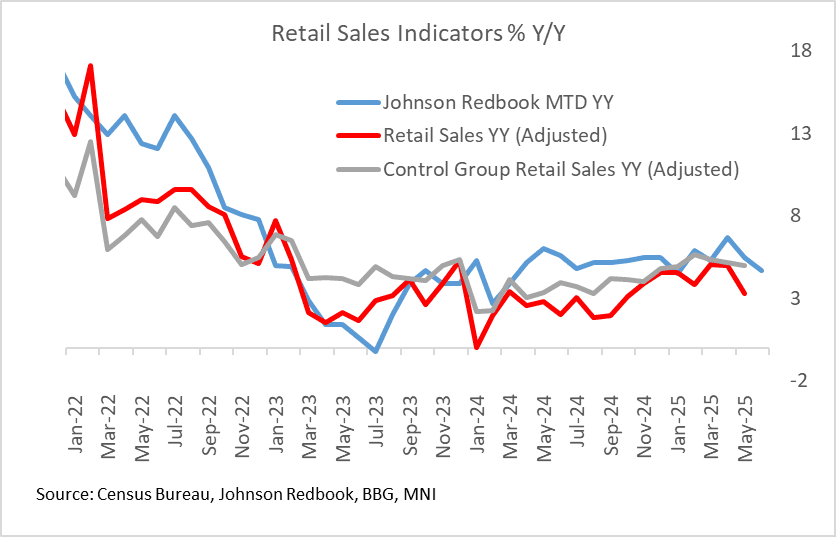

US DATA: Redbook Sales Continue To Suggest Steady Slowdown In Core Retail

Johnson Redbook's retail sales index showed a 5.2% Y/Y rise in the week ending Jun 14, up from 4.7% prior and bringing June-to-date sales to 5.0% Y/Y.

- However that was versus retailers' targeted 5.7% gain, and the report's anecdotals were very much mixed:

- "Father’s Day promotion sales were mediocre, but they still managed to bring customers into stores, increasing foot traffic and creating positive spillover business in other product areas. Off-price and discount retailers continue to gain market share from department stores. During the week, there was notable activity in men’s apparel and other typical gift categories, such as home improvement items, gardening supplies, sporting goods, leisure items, and appliances. Additionally, the summer heat increased customer traffic for seasonal products, including air conditioners, fans, pool and beach equipment, swimwear, and other warm-weather apparel, as most shoppers tended to purchase items according to their immediate needs."

- Redbook's 5.5% Y/Y reading for May exceeded the Census Bureau retail sales report which showed a pullback in overall sales to 3.3% Y/Y, a 7-month low. However that was heavily influenced by weak auto and gasoline sales and other volatile categories, and indeed Redbook was closer to the mark on Control Group sales, which came in at 5.0% Y/Y.

- Both Control Group and Redbook have been seeing a clear but relatively steady slowdown since Q1 on a Y/Y basis, and this looks likely to continue into June.

SOFR OPTIONS: SOFR Put Structure Sales, Call Fly Buying

- -10,000 SFRZ5 95.56/95.68/95.81 put trees, 2.125

- +5,000 SFRZ5 96.25/96.50/96.75 call flys, 2.0 ref 96.11

- -15,000 SFRU5 95.75/95.87 2x1 put spds 2.0 over SFRZ5 95.62/95.75 2x1 put spds

BONDS: Away From Highs After U.S. Data & Crude Uptick

{WO} BONDS: Bonds have traded away from session highs following the U.S. data, as the firmer-than-expected retail sales control group and import prices data countered the initial dovish reaction to softer-than-expected headline retail sales & negative revision.

- A move back towards session highs in crude oil futures also factors in.

- Some focus on a QatarEnergy instruction for ships to wait outside the Gulf until the day before loading, as markets continue to assess energy supply risks stemming from the Iran-Israel conflict.

- Gilts continue to set up for tomorrow’s UK CPI data, where we see downside risks to the headline CPI and services readings.

- Our full data preview is here.

- 48.5bp of BoE cuts priced through year-end, with the next 25bp cut more or less fully discounted through the end of the September MPC (pricing little changed on the day).

- Tsys bull flatten on the day, Bunds twist flatten and gilt see light bear steepening.