OIL PRODUCTS: China’s Fuel Oil Imports Rise 7.3% in June: OilChem

Jul-23 09:50

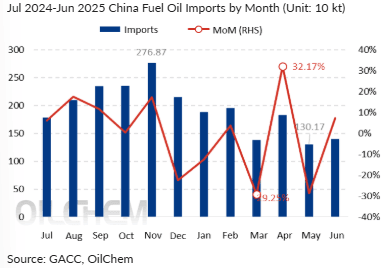

China’s fuel oil imports rose 7.3% on the month in June to 1.40m mt, according to OilChem citing GACC data.

- Jan-June imports totalled 9.74m mt, a rise of 38% on the year.

- June’s import rise was attributed to strong demand from power generation despite a slight drop in local refineries’ operating rates.

- GACC data showed that the import price of fuel oil averaged $461/mt, up 3.1% on the month.

- China is expected ti import 1.5m mt in July, a month-on-month rise of 7.4%. Rising refinery runs is likely to boost fuel oil feedstock consumption.

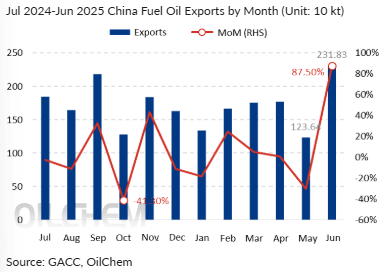

- China’s fuel oil exports were 2.3m mt, up 87.5% on the month. Jan-June exports were 10.1m mt, up 2.4% on the year.

- June volumes were supported by a rise in bunkering volume demand.

- For July, fuel oil exports are seen falling 22.4% to around 1.8m mt.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USD Behaviour Suggests S/T Base Could Be In

Jun-23 09:49

- Greenback rally is holding here despite the more benign market backdrop in response to the US strikes on Iran. The move higher in the USD doesn't look directly headline driven, but participation is decent on the EUR/USD sell-off as the pair tests overnight lows. Headlines on repeated Israeli targeting of the Fordow nuclear site will be pressing for this direction of travel, however.

- It's USD/JPY and GBP/USD that stand out here, however. GBP/USD is through last week's 1.3383 and a close at current or lower levels today would mark the first close below the 50-dma since October last year.

- This price actions plays into the signals of a short-term base of the USD here - and a possible buy-on-dips pattern forming. We noted last week the importance of the USD Index showing above the downtrendline that's defined dollar weakness across Trump's term so far - and noted that even de-escalation headlines were proving insufficient to trigger any material weakness in the USD. This leaves 100.481 - 100.569 area as the next upside target and plausible resistance for a short-term bounce.

FOREX: EURJPY June Advance Increases to 3.7%, CHFJPY at Record Highs

Jun-23 09:47

- While AUD and NZD have also been bearing the brunt of G10 FX declines alongside the Japanese Yen on Monday, the relative outperformance for the likes of EUR and especially CHF are providing notable boosts for some of the yen crosses.

- EURUSD’s resilience around the 1.15 region has allowed EURJPY to extend its rally this month to 3.7%. Price action has been exacerbated by the notable climb back above 168.00 to trade at 11-month highs for the cross, narrowing the gap substantially to 170.00 and 170.47, a key Fibonacci retracement point. It is worth highlighting that the cross is overbought, and a pullback would unwind this condition.

- In similar vein, CHFJPY gains total 3% in June, with recent strength underpinned by the pair reaching an all-time high above the psychological 180.00 mark. Last week’s comparatively hawkish SNB may be providing an additional tailwind here (review here).

- Additionally, the current trajectory highlights how the Franc may be the preferred option in times of geopolitical turmoil, while JPY is seen as a more rate-sensitive haven. A further deterioration of middle east conditions in the form of extensive Iranian retaliation could thus provide further upside potential here. On the upside, projection levels of note from the Apr 25 - May 13 - May 23 price swing are 181.35 and 182.32.

EGBS: Bund Futures Remain Sensitive To Mid-East Developments

Jun-23 09:46

Bund futures are -7 ticks at 130.86, with markets still sensitive to developments in the Middle East after the US attacked Iranian missile sites over the weekend. Israeli attacks on Tehran and the Fordow nuclear facility have continued today, but our commodities team notes that there are no signs that Iran is ready to carry out threats to block oil shipments.

- Bunds remain in consolidation mode and continue to trade below the Jun 13 high. For now, the latest move down appears to be a correction. Key short-term support to watch lies at 130.12, the Jun 5 low.

- German yields are 1-2bps higher, with the 5-year tenor underperforming.

- 10-year EGB spreads to Bunds are within 0.5bps of Friday’s closing levels (with the exception of GGBs, +1.5bps wider). Early narrowing has unwound with European equity futures now off session highs.

- The EU sold 5/10/25-year EU-bonds this morning, with Belgium also scheduled to sell OLOs at 1100BST. Slovenia announced a mandate for a 10-year benchmark.

- The Eurozone flash June services PMI ended up in line with consensus at 50.0 (vs 49.7 prior), somewhat surprising given the German reading was 1.6 points stronger-than-expected and France was only 0.3 points below consensus. This suggests that although the Eurozone ex-Germany and France continues to outperform the two largest economies, momentum in activity levels appears to be converging.

- ECB President Lagarde speaks at EU Parliament at 1400BST, with Nagel speaking on regulation at 1600BST.

- Elsewhere, there is some attention on the outcome of today’s French pension reform negotiations and tomorrow’s German budget/issuance plan.