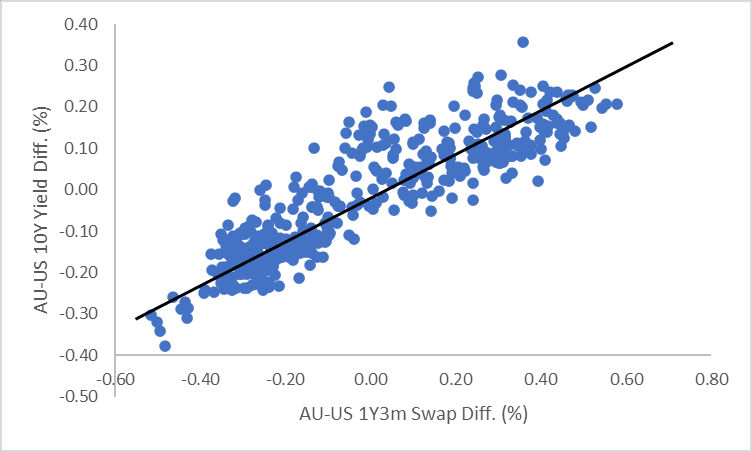

AUSSIE BONDS: AU-US 10Y Diff Sits In Bottom Half Of Range

The AU-US 10-year cash yield differential currently stands at -16bps, positioned near the bottom of the +/- 30bps range that has largely held since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past year suggests the current spread is slightly below fair value at -12bps.

- The 1Y3M differential, a key gauge of expected relative policy trajectories over the next 12 months, has traded within a 40bp range this year and is currently near the middle of the range at ~-20bps.

- In early February, the 1Y3M differential had declined approximately 100bps since mid-September 2024, falling from +60bps to -40bps.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: MNI - Market News / Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GLOBAL MACRO: March Exports Jump Ahead Of US Tariffs, Especially From Asia

The March CPB global trade data showed a significant pickup in export growth as countries, especially in Asia, try to beat the imposition of US duties. Reciprocal tariffs were announced on April 2 and then delayed until July 9 to allow negotiations to take place. Exporters are likely to continue front loading shipments in case agreements are not reached, increasing inventories and thus the likelihood of a drop in trade in H2.

- Global trade rose 2.2% m/m in March to be up 6.6% y/y, fastest since December 2021, after 0.5% & 3.0% in February. Exports rose 2.3% m/m and 5.9% y/y up from 2.0% y/y with both DM and EM posting monthly increases. The Baltic Freight Index and manufacturing PMI suggest there will be a correction.

Global trade y/y% vs Baltic Freight Index

Source: MNI - Market News/LSEG

- Shipments from developed markets rose 1.2% m/m and 3.9% y/y after 1.4% y/y. This was the fifth consecutive monthly rise. Advanced Asia saw exports increase 12.1% y/y, while Japan’s rose 6.6% y/y. The euro area rose 0.5% y/y, highest since November 2022, and the US by 4.3% y/y.

- EM Asia also saw strong export growth with China up 16.9% y/y and excluding China +6.4% y/y. Latin America increased 10.2% y/y. Mexico received some reprieve from US duties through USMCA-compliant goods worth around half of US imports from Mexico but still faces universal tariffs on steel and autos. Overall EM exports rose 3.7% m/m to be up 9.1% y/y following February’s 3.1% y/y.

Global exports y/y%

CHINA: Bond Futures Rise Post Liquidity Injection

- China's bond futures are up today following the PBOC injection of liquidity via this morning's open market operations.

- The 10YR future is up +0.04 to 108.89 as it trades through the 20-day EMA of 108.85 for the first time this month.

- The 2YR future is up +0.02 to 102.42 and remains below all major moving averages; the nearest being the 20-day EMA of 102.47.

- The 10YR CGB is stronger this morning at 1.68%, from Friday's close of 1.69%

- The key data out this week for China is Industrial Profits for April and PMI's

JGBS: Bull-Flattener At Lunch, Subdued Session With US Tsys Out

At the Tokyo lunch break, JGB futures are holding onto gains, +14 compared to the settlement levels, but off session bests.

- US equity-index futures have climbed in early Asian trading after President Donald Trump extended a deadline on aggressive European tariffs. Trump agreed to delay the date for a 50% tariff on goods from the European Union to July 9 from June 1.

- US tsy futures (TYM5) have weakened in early Asia-Pac dealings, with TYM5 at 109-27+, -0-07 from closing levels. Cash US tsys are closed today for Memorial Day.

- “Japan may offer financial and technical contributions to the US, including investment in an Alaskan LNG pipeline project and shipbuilding expertise, to smooth the path toward a tariff deal by mid-June. Japan's Prime Minister Shigeru Ishiba hopes to reach an agreement in time for a planned bilateral meeting with Donald Trump at the Group of Seven summit in Canada next month.” (per BBG)

- Cash JGBs are little changed across benchmarks out to the 5-year but to 1-2bps richer beyond, with a flattening bias. The benchmark 30-year yield is 2.1bps lower at 3.032% versus the high of 3.204%. It was as low as 3.0% earlier in the session.

- Swap rates are 2-5bps higher. Swap spreads are wider.