CHINA PRESS: Additional Policies Expected In H2 - Analysts

China should consider front-loading next year’s government bond quota to address local government implicit debt and help offset the shortfall in government bond supply expected in the final quarter, according to Ming Ming, chief economist at CITIC Securities. Authorities need to expand overall liquidity injections and reduce benchmark interest rate in the second half, Ming added. The use of unsold units purchased by authorities should be expanded to cover long-term rental housing and apartments for skilled talent, accompanied by more flexible eligibility criteria, said Yuan Haixia, president of China Chengxin International Research Institute. (Source: China Securities Journal)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

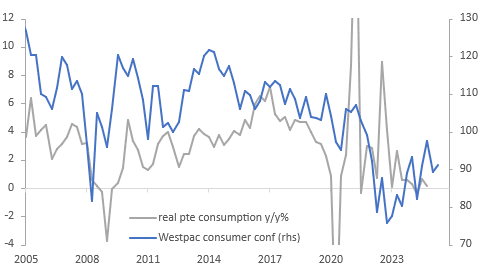

NEW ZEALAND: Westpac Consumer Confidence Signals Spending Outlook Remains Soft

Westpac Q2 consumer confidence picked up to 91.2 from 89.2 in Q1, while the number of pessimists declined they continue to outnumber optimists with the breakeven-index 100. Sentiment also remains below Q4 2024’s 97.5. Households remain cautious about the outlook despite 225bp of RBNZ easing given heightened global uncertainty, an unbalanced recovery and a soft labour market.

- While most regions saw a rise in consumer confidence, only one posted a reading above 100.

- Present conditions remained weak at 81.7 up from 80.2 with the assessment of current financial conditions falling to -27 from -24.1. Westpac notes that finances are being impacted by rises in living costs. Q1 CPI inflation rose 2.5% y/y up from 2.2% while May data showed food and electricity inflation rising further.

- The outlook is more positive with expected conditions rising 2.3 points to 97.5, still below the 10-year average, and the expected financial situation improving 2.6 points to 7.4.

- It is still not a “good time to buy” a major item but it improved 6.1 points to -9.5 but the 10-year average is at +4.5. Recent consumption data have been lacklustre and show that households remain cautious. The Westpac survey found that a net 31% have reduced discretionary spending.

NZ consumer outlook

AUSTRALIA: May Unemployment Rate Expected To Stay At 4.1%

May jobs data are released on Thursday and Bloomberg consensus is expecting labour market tightness to continue, one of the reasons the RBA remains cautious regarding the monetary policy outlook. Consensus is forecasting a 21.2k increase in new jobs, close to the 3-month average of 23k, with the unemployment rate is steady at 4.1%. In May the RBA projected 4.2% in Q2 and employment growth of 2.1% y/y.

- Employment forecasts are between +40k and -20k with most around +10k to +30k. ANZ and NAB are above consensus expecting 25k and 30k respectively, while CBA is slightly below at 20k and Westpac at 15k is the most pessimistic of the big four local banks.

- New jobs rose a stronger-than-expected 89k and 2.7% y/y in April. The data were released May 15, the day after the RBA cut off for its forecasting round. Thus, its 2.1% Q2 2025 projection looks too low and would require employment to fall 50k in both May and June.

- The unemployment rate was a low 4.1% in both March and April at 4.05% and 4.07% respectively. Consensus is very narrow with 20 analysts expecting it to remain at 4.1% and 7 a rise to 4.2%. ANZ, NAB and CBA forecasts are at 4.1%, while Westpac has it rising to 4.2%.

- To achieve the RBA’s average 4.2% in Q2, the unemployment rate would need to rise 0.1pp in both May and June.

- The participation rate is projected to be unchanged at 67.1% in May. It rose 0.3pp in April.

JGBS: Twist-Steepener As Yesterday's BOJ Taper Decision Is Digested

At the Tokyo lunch break, JGB futures are stronger and hovering near session highs, +33 compared to the settlement levels.

- Japan’s April core machine orders fell sharply, but in line with market projections. We were down -9.1%m/m (-9.5% forecast and following a 13.0% gain in March).

- Japan's May trade data was close to expectations, with export growth at -1.7%y/y, versus -3.7% forecast. The April outcome was +2.0%. On the import side, we were -7.7%y/y, against a -5.9% forecast (-2.2% was recorded for April). The trade deficit was -¥637.6bn, close to forecasts but wider than the -¥115.6bn print in April.

- Cash US tsys are slightly cheaper in today’s Asia-Pac session after yesterday’s bull-flattener.

- “JGB futures are firm in early business, helped by the bid for Treasuries, but Japanese bonds won’t be getting much of a haven bid as the BOJ isn’t finished with hiking rates. Traders have parsed Governor Ueda’s language during his press conference and it is clear that the job of removing unconventional monetary policy is far from complete.” (per BBG)

- The cash JGB curve has twist-steepened, with yields 2.5bps lower to 2.5bps higher. The benchmark 10-year yield is 1.5bps lower at 1.45% versus the cycle high of 1.596%.

- The swaps curve has also twist-steepened, with rates 1bp lower to 2bps higher.