SONIA OPTIONS: Adding to the large Call Condor

SFIU6 96.10/96.20/96.25/96.35c condor, bought for 5.25 and 5.5 in 30k total....

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

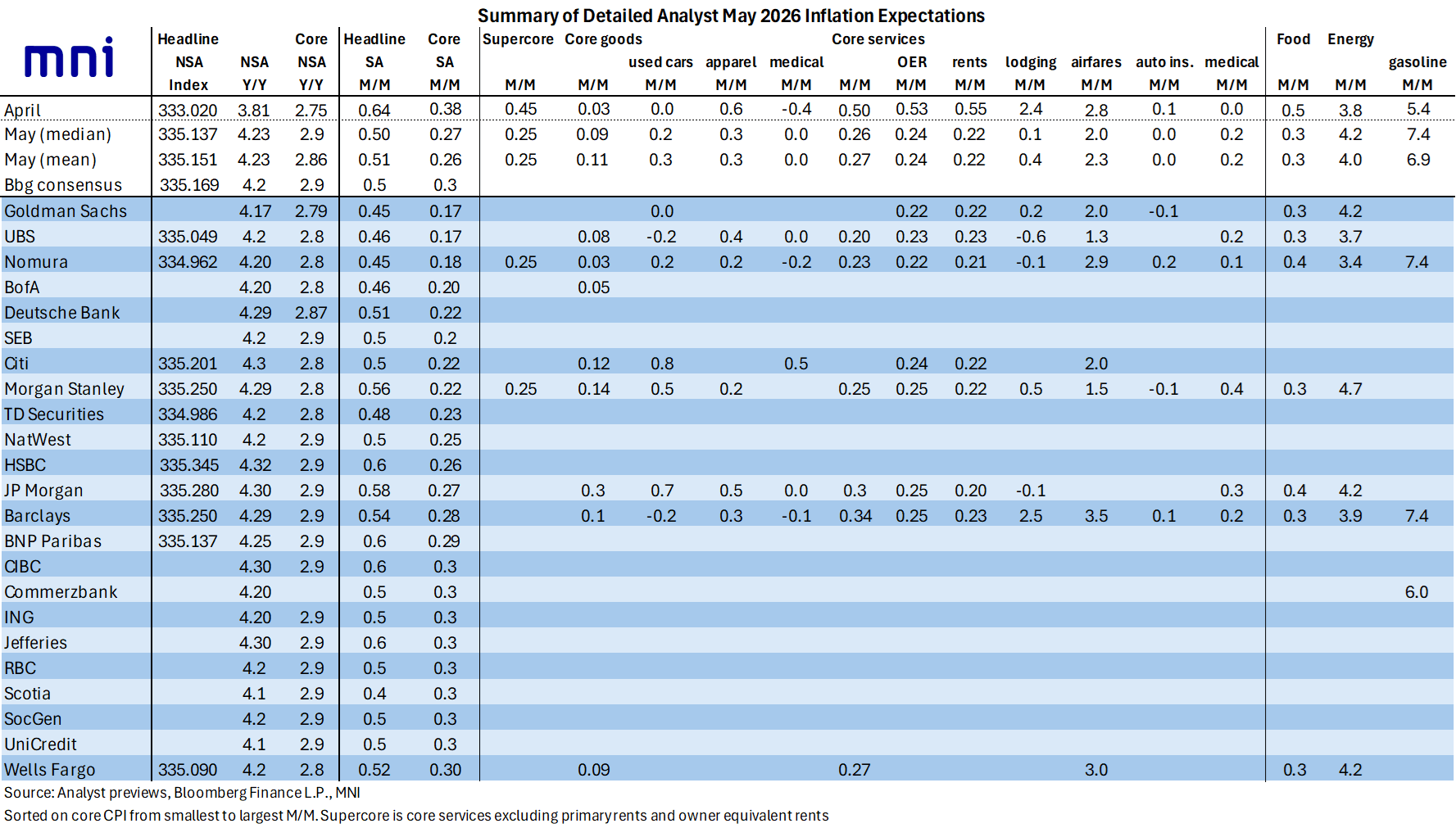

US INFLATION: Analyst Expectations Of Key Sequential Drivers For May CPI Report

Energy inflation should see a similarly strong increase as in April but food might moderate after a strong April:

- Energy (small +ve to neutral): Energy prices are expected to show another strong increase of ~4.0% M/M (range 3.4-4.7%) after 3.8% M/M in April following the booming 10.9% M/M in March.

- Food (-ve): Expected to moderate to 0.3% M/M after a surprisingly strong 0.5% M/M in April, which had in turn been driven by the food at home category jumping 0.68% M/M (highest since Aug 2022) in a potential sign of passthrough from higher transportation and fertilizer costs.

For core, upside drivers to M/M inflation compared to April are relatively limited with highlights being used cars and medical items. Largest downside drivers are rents – after an artificial boost in April – and lodging away from home.

- Used cars (+ve): Expected to firm after a surprisingly soft April, with an average 0.3% M/M in May but a reasonably wide range of -0.2% to 0.8% M/M. Feedthrough from prior strength in the Manheim used vehicle series has been slow.

- Medical items (+ve): Medical care commodities are on average seen flat after slipping -0.4% M/M in April whilst services could have firmed a little after a flat April.

- Rents (large -ve): OER and primary rent inflation should drop back to typical monthly rates in May after a delayed impact from last year’s government shutdown saw a sharp acceleration in April. OER on average seen rising 0.24% M/M in May (range 0.22-0.25) after 0.53% in Apr and 0.28% in Mar, primary rents seen rising 0.22% M/M (range 0.20-0.23) after 0.55% in Apr and 0.19% in Mar. Recall that because the sample from 6 months earlier wasn’t available in April, the BLS looked at the 12-month change for inflation in the sample and used the 6th root of that change (as opposed to the 12th root).

- Lodging (large -ve): Seen moderating notably after being easily the largest surprise in the April report, on average seen riding 0.4% M/M (median 0.1) after a much stronger than expected 2.4% M/M in April. It’s not a uniform view, with an analyst range of -0.6% to 2.5% M/M.

- Airfares (-ve): On average seen rising 2.3% M/M (median 2.0) after the 2.8% M/M in April had somewhat underwhelmed strong expectations as a sharp increase in jet fuel prices continues to feed through. The analyst range of 1.3-3.5% is on the narrower side for this volatile category that doesn’t feed into PCE.

- Apparel (-ve): On average seen rising 0.3% M/M after a surprisingly robust 0.6% M/M in April considering it had already seen two very strong increases of 1.0% in March and 1.3% in Feb in what was its strongest single month since 2018.

[A quick reminder that the below table shows median/mean figures across all estimates, hence the core CPI median of 0.27% M/M vs the 0.23% if only taking unrounded estimates per the separate table shown later.]

AUD: FX Exchange traded

AUDUSD (2nd July) 72.00c, bought for 0.11 in 1.6k.

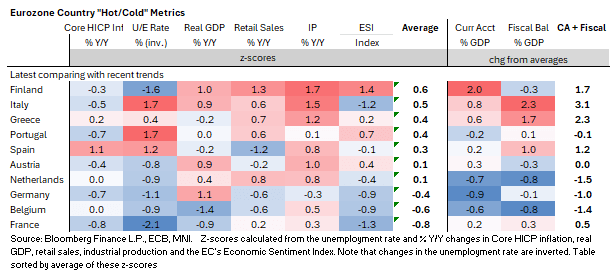

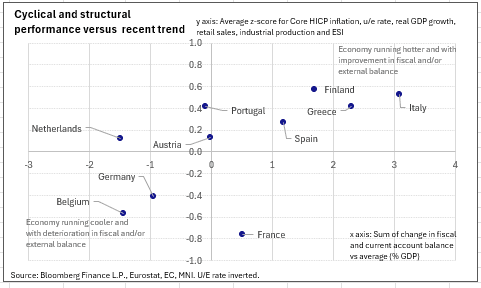

EUROZONE DATA: Finland A Surprising Cyclical Leader In Our Latest Heatmap Update

Ahead of this week’s ECB decision, we refresh our simple heatmaps on cyclical and structural economic performance across the largest Eurozone economies. Southern European countries continue to outperform from a cyclical perspective, with Finland joining them in the latest iteration. Meanwhile, Belgium, France and Germany remain laggards.

- Finland position on our heatmaps is interesting, given the pessimistic narrative around recent increases in the unemployment rate (which is now notably above Spain at 11.6%). Unemployment is indeed a drag on our heatmaps, but improving momentum in retail sales, industrial production, sentiment and real GDP have provided an offset (all on a Z score basis vs the prior 3 years).

- In a speech last month, Bank of Finland Governor Olli Rehn noted that growth had been surprisingly strong in Q1, and that Finland is somewhat insulated from the Iran war energy shock due to its low reliance on oil/gas. He also noted that “Turku Shipyard announced an order for two large cruise ships and Kone announced its historic major acquisition. This news is cause for joy and we hope that it will also improve consumer confidence in the economy in an uncertain situation.”

- Belgium and France remain at the bottom of our leaderboard, with labour market, real activity and sentiment series weighing. Structural metrics also remain a source of weakness - both run large fiscal deficits alongside smaller current account deficits. In France, markets will be cognizant of returning political risks in H2, as 2027 budget and Presidential Election newsflow starts picking up.

- Most analysts still expect increased public spending to strengthen German growth this year (providing some offset to the Iran war shock). However, for now the impulse has been lacking, and today’s weak factory orders print supports this trend.